At Ozone API our mission is to help banks and financial institutions deliver high performing open APIs, so they can meet regulatory requirements and drive their strategies for creating revenue through value adding and premium APIs.

Our background has involved creating a number of the leading global open banking standards so we have a fairly unique insight. But in building our platform to support all global standards we have made some interesting observations.

1. The global standards landscape is getting more, rather than less, fragmented

With markets around the world delivering open banking and open finance, we are seeing more standards and variants of standards emerging.

This is usually for good reason as each market may be doing it with slightly different objectives in mind, for example to tackle financial inclusion, drive investment and growth, while accelerating innovation in financial services.

These different drivers may result in varied frameworks focusing on different key enabling use cases. And this is leading to new variances of these standards.

As mentioned, this can be a good thing, accelerating the innovation around standards and creating new capabilities (see the chart below). But it certainly increases the complexity for banks with multiple global standards that are also continually changing. Learn more by exploring The Global Open Data Tracker to see the evolving ecosystem of global open finance standards.

2. There are more similarities than differences

Whilst it’s true that the standards landscape is seeing fragmentation and different variances, it’s also true that a lot of the core foundations are similar, creating a good path for interoperability.

For example:

Firstly, many concepts are very similar – for instance account information and payment information – although they can diverge quickly at the level below (e.g. approach to payment initiation)

Increasingly most of the more modern and mature standards are based on the OpenID Foundation’s FAPI security protocols. That said, there are currently five different versions and 25 possible combinations, which creates a base for interoperability and a more consistent approach to consent management and security

3. Change is a constant

Open banking is definitely not a case of “build it once and you’re done”. Most of the standards continue to evolve as the regulatory frameworks and market demands evolve. This results in regular updates to standards, bringing improvements and new functionality.

In some markets that may happen in fairly structured major and minor releases a few times a year. In other markets (Brazil being a case in point) change is almost constant with an ongoing cycle of updates and re-certification across open finance and open insurance every few weeks.

Doing it well means staying at the sharp end of the spear and constantly evolving to keep up with the evolution (and sometimes revolution) in the standards space.

4. Between them they deliver a LOT of capability

We’re helping to power open banking for many banks around the world from Latam to Australia and everywhere in between. In doing so we’ve built our platform so we can simply and rapidly add any new global standard and keep it up to date.

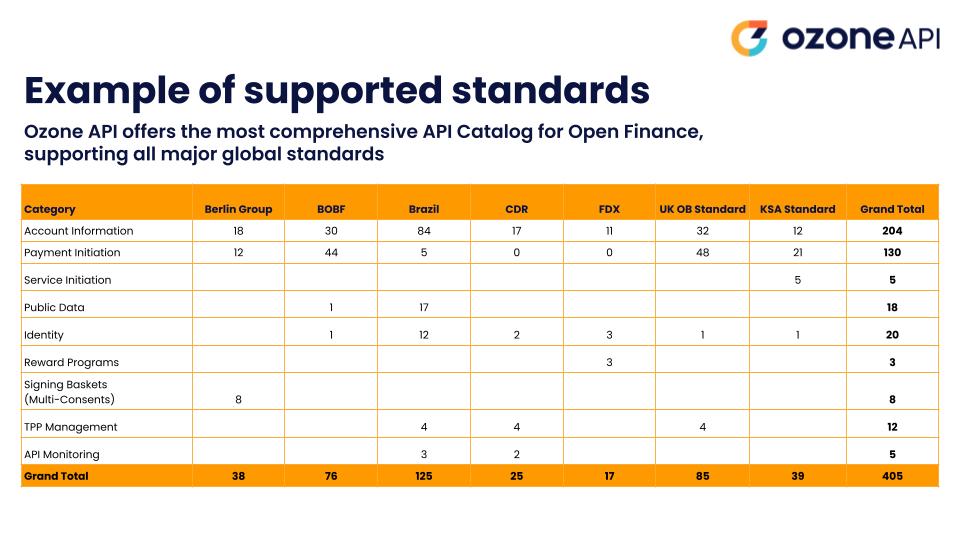

When we look at the range of standards it’s remarkable the amount of capability and extent of APIs that are enabled.

The chart below compares just some of the standards that we are supporting on behalf of our banks and partners. And the numbers continue to increase all the time.

5. The standards are starting to deliver capabilities that can really help drive value for banks and FIs

The key discussion we have with banks around the world is how they can use open APIs to really create value and deliver better financial experience for their customers. As we look at the breadth of capabilities across the standards it already creates a rich menu of capabilities.

We’re working with banks and financial institutions around the world to help them take advantage of the capabilities and to build new ones. Typically in areas like:

Account information

Enriched account information

Identity assertions

Payment initiation

Variable recurring payments

Bulk / batch payments

X-border and FX payments

Service initiation

Account opening / new product set up

Change of details

This is heading in one direction, and we’ll see the global menu of standards cater to the needs of most banks in the near future.

Conclusion

For us to ensure we can enable our customers and partners around the world to deliver the most comprehensive open banking strategies, our mission is to continue to both shape and support the wide array of global standards.

In doing so we take away the complexity AND deliver a much more future proofed platform for any bank or financial institution.

One thing is certain, the landscape will continue to become both more complex and more enabling.

Get in touch to speak to one of our open finance experts.

The FCA has published its Open Finance Roadmap, with key milestones beginning this year and a 2030 horizon. Banks, lenders, and fintechs face a significantly wider scope than open banking, with real commercial opportunity for those who prepare early. Here is what the roadmap says and what it means for your business.

The FCA has published its Open Finance Roadmap with specific milestones, credible use cases, and an honest acknowledgement that the UK is catching up, not leading. We break down what the plan gets right, where the real risks are, and what regulators worldwide should take from it.

In September 2024, I published Global Interoperability, making the case that open finance would only deliver on its promise if the underlying plumbing was standardised globally, not just market by market. Eighteen months later, the landscape has changed considerably. More markets. More data. More urgency. Three arguments from that piece have aged particularly well, and...

Huw Davies

Huw Davies